Leveraging a non-occupant co-borrower to buy a home

For first-time homebuyers, qualifying for a mortgage loan can be a challenge, especially if their income, credit score or debt-to-income ratio falls a bit short of their lender’s requirements. However, they do have options.

One way to increase the chances of getting their mortgage application approved is to have family member or friend sign on as a non-occupant co-borrower.

A non-occupant co-borrower is someone who signs for a mortgage loan alongside the primary borrower but does not plan to live in the home that’s being financed. Like a co-signer, a non-occupant co-borrower is responsible for mortgage repayment if the primary borrower defaults.

Just like the primary borrower, lenders take into consideration the co-borrower’s income, credit history and existing debts, so if their debt obligations are too high, they may not be able to help the borrower qualify for the loan.

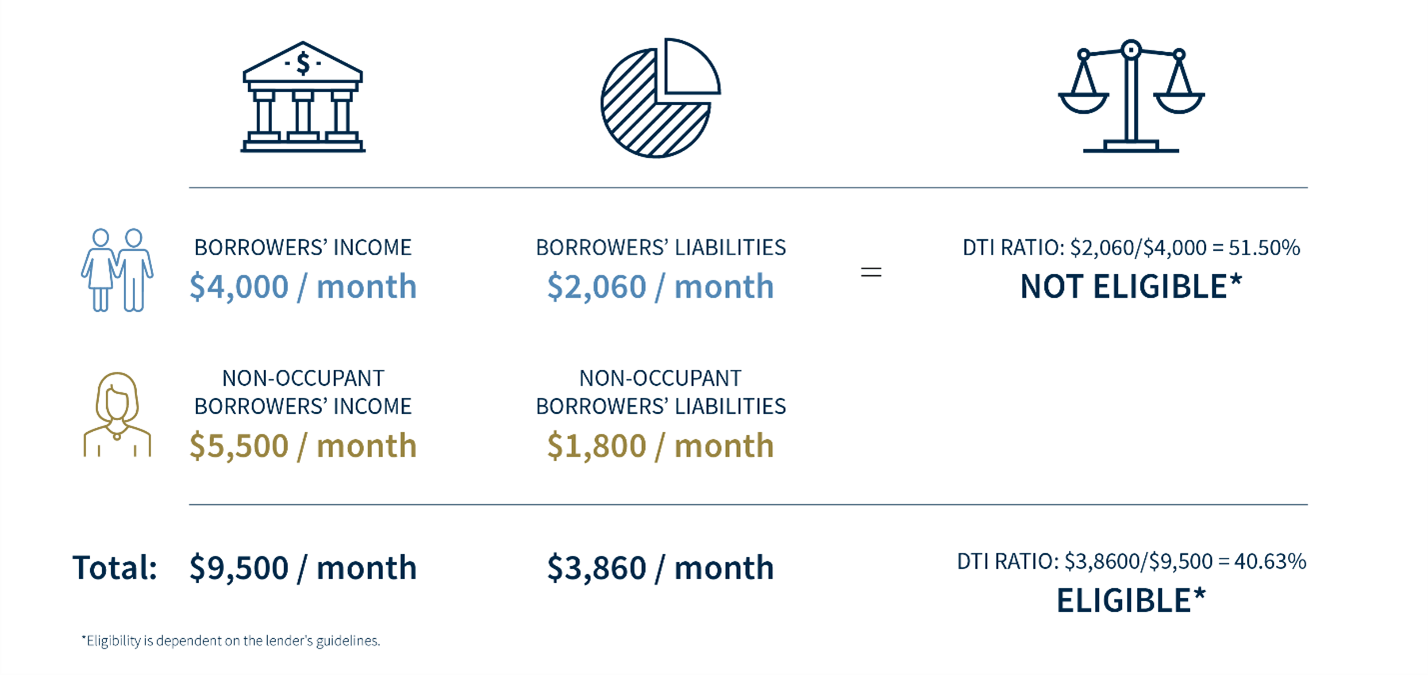

For example, say a young couple wants to buy their first home, but with $50,000 in student loans, their debt-to-income (DTI) ratio – their total monthly payments divided by their gross monthly income – is too high to qualify for a loan.

But if his mother signs on as a borrower on the mortgage, the lender now also includes her income and liabilities in the DTI ratio.

This strategy provides a multigenerational benefit: The mother can invest in an asset that may grow over time and the son can buy a home of his own. If the non-occupant co-borrower wishes to be removed from the loan at a later date, the homeowner may be able to refinance the home solely in their name.

Most often a parent or other close relation to the borrower, a non-occupant co-borrower is fully responsible for the loan, which does have potential drawbacks. For example, their credit will be negatively affected by missed or late payments. It could even reduce the chances of the parent obtaining their own mortgage or other type of loan, because the home being financed will be included in their own DTI ratio.

While non-occupant co-borrowing is still relatively unknown as a viable solution, it may become a more popular option in the future. With the average student debt balance near $40,000, a family co-borrower could help make a young family’s dream of homeownership a reality.

Your financial advisor can connect you with a mortgage consultant to discuss whether signing on as a co-borrower is suitable for your situation.

Sources: Fannie Mae, Homebuyer.com, Mortgage Research Center, Guardian Mortgage, Education Data Initiative

Lending Services provided by Raymond James Bank, member FDIC, NMLS ID #405712. Raymond James & Associates, Inc., and your Raymond James Financial Advisor do not solicit or offer residential mortgage products and are unable to accept any residential mortgage loan applications or to offer or negotiate terms of any such loan. You will be referred to a qualified Raymond James Bank employee for your residential mortgage lending needs.